🏦 Revolving Loans — A Comprehensive Guide

- Introduction

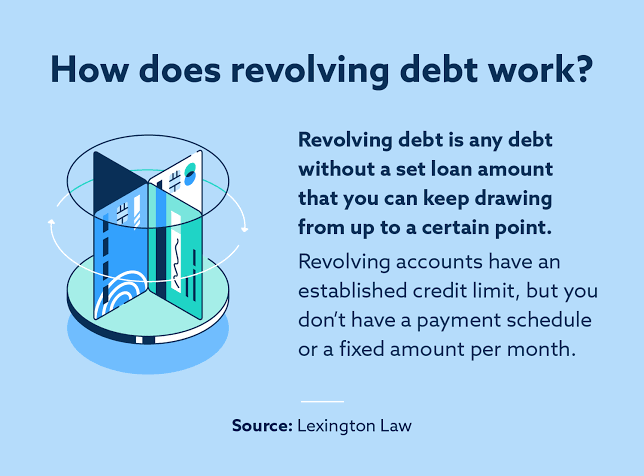

Revolving loans are a category of credit arrangements where the borrower has continuous access to funds up to a certain limit and can reuse the credit as it is repaid. Unlike traditional term loans, which provide a lump sum with fixed repayment terms, revolving loans operate more like an ongoing credit facility — funds revolve in and out as needed.

They are widely used by individuals, businesses, and even governments for managing cash flow, meeting unexpected expenses, or financing ongoing operations. Examples include credit cards, personal lines of credit, and business revolving credit facilities.

- Key Characteristics

Here are the defining features of revolving loans:

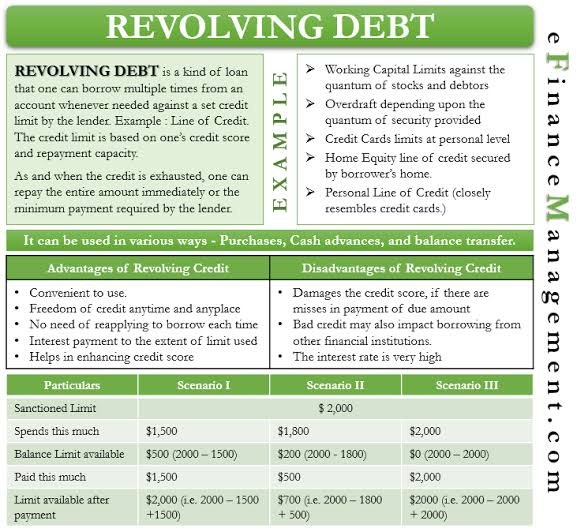

- Credit Limit: A maximum amount the borrower can draw from at any time.

- Reusability: Funds become available again once repayment is made.

- Variable Usage: Borrowers can choose how much to use and when.

- Flexible Repayment: Minimum monthly payments are common, though paying the full balance is often financially prudent.

- Interest Charges: Interest is generally applied only to the amount actually borrowed.

- No Fixed End Date: Facilities may remain open as long as both lender and borrower agree, subject to periodic reviews.

- Types of Revolving Loans

Revolving loans can be classified into consumer and business categories.

A. Consumer Revolving Loans

- Credit Cards 💳: The most common example. Funds can be used for purchases, balance transfers, or cash advances.

- Personal Lines of Credit: Offered by banks, giving individuals access to a pool of funds for emergencies, renovations, or education.

- Home Equity Lines of Credit (HELOCs): Secured by property, providing access to a credit line based on home equity.

B. Business Revolving Loans

- Business Lines of Credit: For working capital, purchasing inventory, or covering seasonal fluctuations.

- Overdraft Facilities: Linked to business accounts to cover short-term cash shortfalls.

- Trade Finance Credit Lines: Supporting import/export activities.

- Advantages

Revolving loans offer significant benefits:

- Flexibility: Borrow only what is needed, when it’s needed.

- Cash Flow Management: Ideal for smoothing income and expense mismatches.

- Reusable Credit: No need to reapply for a loan once approved.

- Emergency Access: Funds are available quickly for urgent needs.

- Credit-Building Tool: Responsible usage can improve credit scores.

- Disadvantages and Risks

While revolving credit is convenient, it carries potential drawbacks:

- Higher Interest Rates: Especially on unsecured facilities like credit cards.

- Debt Accumulation Risk: Easy access can lead to overspending.

- Variable Rates: Payments may rise if interest rates increase.

- Minimum Payment Trap: Paying only the minimum leads to long repayment periods and high interest costs.

- Annual/Service Fees: Many lenders charge maintenance fees.

- How Interest Works

Interest on revolving loans is generally calculated based on the average daily balance during the billing cycle. For example: - Borrow ₹100,000 for 15 days at 18% annual interest.

- Interest formula:

[

Interest= Principal x Rate x Days/365

] - Calculation: ₹100,000 × 0.18 × (15/365) ≈ ₹739.73

This means you only pay interest for the time and amount borrowed.

- Revolving vs. Non-Revolving Credit

Feature Revolving Credit Non-Revolving Credit

Borrowing Limit Reuse Yes No

Repayment Structure Flexible Fixed installments

Examples Credit card, LOC Car loan, mortgage

Approval Needed for Reuse No Yes- Use Cases

Revolving loans are valuable in many scenarios:

- For Individuals: Managing seasonal expenses (festivals, holidays), emergency repairs, medical bills.For Businesses: Covering gaps between accounts receivable and payable, funding short-term projects.For Governments: Bridging cash flow timing gaps in tax collection and spending.

- Best Practices for Borrowers

To use revolving loans wisely:

- Borrow Strategically: Use funds for productive purposes, not impulse spending.Pay More Than the Minimum: Reduces interest costs and frees up credit faster.Monitor Credit Utilization Ratio: Keep usage below 30% of the limit for better credit health.Compare Fees and Rates: Shop around for the most cost-effective facility.Review Terms Annually: Lenders may change rates, fees, or conditions.

- Regulatory Aspects in India

In India, revolving credit facilities like credit cards and personal lines of credit are regulated by the Reserve Bank of India (RBI). Key points:

- Disclosure norms on interest rates and fees.Guidelines to prevent predatory lending.Requirements for transparent billing practices.Credit bureaus track usage and repayment behavior, influencing a borrower’s credit score.

- Economic Impact

Revolving loans are a double-edged sword in the economy:

- Positive: Stimulate spending, smooth consumption, and support business continuity.Negative: Can contribute to household debt stress and defaults if mismanaged, especially in low-interest-rate boom cycles followed by tightening.

- Conclusion

Revolving loans are not just a financial tool — they’re a test of financial discipline. The same flexibility that makes them convenient can also lead to financial strain if borrowers aren’t cautious. For both individuals and businesses, the key is to balance accessibility with responsibility, treating revolving credit as a liquidity buffer rather than a source for long-term debt.

- Use Cases

- 💡 Final Thought:

Think of a revolving loan as a financial Swiss Army knife — versatile, handy, and potentially lifesaving in a pinch. But, like any sharp tool, it works best in the hands of someone who knows when and how to use it. Dex, if you’d like, I can also prepare a visually appealing infographic summarizing these points for quick reference — it could be useful for study or presentation. Would you like me to do that next?