💍 Wedding Loans: A Comprehensive Guide

- Introduction

A wedding is one of life’s most cherished milestones — and often, one of its most expensive. From venue bookings and catering to attire and photography, the costs can add up quickly. For many couples and families, personal savings alone may not be enough.

Enter the wedding loan: a personal loan specifically used to finance wedding-related expenses. Though not a separate loan product in most cases, a wedding loan is essentially a personal loan with the declared purpose of funding a wedding.

- What is a Wedding Loan?

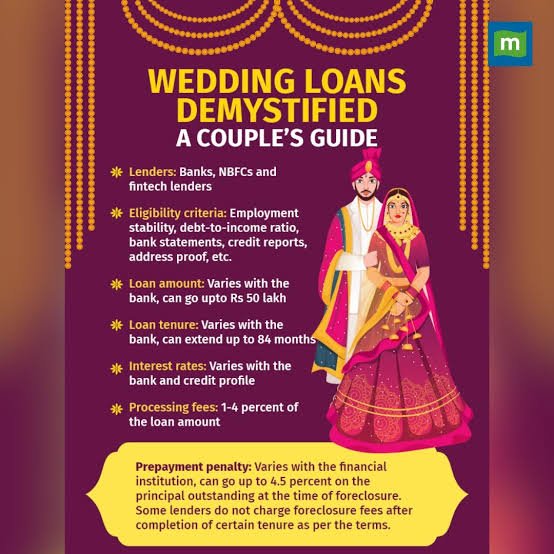

- Definition: An unsecured personal loan taken to cover wedding expenses. The borrower receives a lump sum and repays it in fixed monthly instalments over a set tenure.

- Loan Type: Unsecured — meaning no collateral (like property or gold) is required.

- Amount Range: Varies by lender and eligibility; can range from ₹50,000 to ₹25,00,000 or more in India.

- Tenure: Typically 12 to 60 months.

- Interest Rate: Generally between 10% and 24% p.a. in India, depending on credit score, income, and lender.

- Why Opt for a Wedding Loan?

- Bridge the Funding Gap: When savings and family contributions fall short.

- Preserve Liquid Assets: Avoid dipping into emergency savings or investments.

- Flexibility: Funds can be used for any wedding-related expense — décor, catering, gifts, honeymoon bookings, etc.

- Quick Disbursal: Many lenders offer same-day or next-day disbursal for eligible applicants.

- Key Features

Feature Description

Unsecured No collateral required.

Fixed EMIs Predictable monthly payments make budgeting easier.

Flexible Usage Covers varied expenses, from major bookings to last-minute costs.

Prepayment Facility Some lenders allow early closure with minimal charges.

Online Application Most banks and fintech lenders process applications digitally.- Eligibility Criteria

While specifics vary by lender, common requirements include:

- Age: 21 to 60 years.Income: Minimum ₹15,000–₹25,000 monthly (varies).Employment: Salaried or self-employed with proof of income.Credit Score: 650–750+ improves approval chances.Residence Stability: Often requires at least 6–12 months at current address.

- Documents Required

- KYC: Aadhaar, PAN, Passport, or Voter ID.Income Proof: Salary slips, bank statements, or ITR (for self-employed).Address Proof: Utility bills or rental agreement.Employment Proof: Offer letter, employee ID, or business license.

- Costs and Charges

Beyond interest, be mindful of:

- Processing Fee: 1%–3% of loan amount.Prepayment Charges: 2%–5% (if applicable).Late Payment Fee: Fixed amount or percentage per missed EMI.GST: Applicable on processing and other charges.

- Benefits of a Wedding Loan

- ✅ No Collateral Risk: Property and assets stay untouched.✅ Faster Approval than secured loans.✅ Structured Repayment Plan for easy budgeting.✅ Improves Credit Mix if repaid on time.✅ Convenient Access with minimal paperwork.

- Drawbacks & Risks

- Eligibility Criteria

- Tips Before Taking a Wedding Loan

- Set a Realistic Budget: Fix the total spend before borrowing.

- Borrow Only What’s Needed: Cover the gap, not the entire cost if possible.

- Compare Lenders: Look at rates, tenure, fees, and reviews.

- Check Eligibility Pre-Approval: Avoid multiple hard inquiries on your credit report.

- Plan EMI Affordability: Ensure payments won’t strain your finances post-wedding.

- Negotiate Rates: Loyal customers or those with high credit scores may secure better terms.

- Alternatives to Wedding Loans

- Savings: Most cost-effective, interest-free option.

- Borrowing from Family/Friends: Flexible repayment, but can strain relationships.

- Secured Loans: Lower rates if you’re comfortable pledging an asset.

- Credit Cards: Useful for small, short-term expenses (but high interest if unpaid).

- Example Scenario

Imagine you need ₹10 lakh for your wedding but only have ₹7 lakh in savings.

A personal wedding loan for ₹3 lakh at 12% p.a. over 3 years would cost you:

- EMI: ~₹9,958 per month.

- Total Interest Paid: ~₹58,488.

- Total Repayment: ~₹3,58,488.

- Final Thoughts

A wedding loan can be a practical solution for couples aiming to make their big day memorable without immediate financial strain. However, the joy of the occasion should be balanced with financial prudence. Borrowing for a celebration is fine — as long as repayment is comfortably manageable, and the loan supports, rather than overshadows, the happiness of married life.

💡 Smart borrowing ensures that your first year of marriage is filled with love and joy — not financial stress.