Balloon Mortgages: What They Are, How They Work, and When They Make Sense

A balloon mortgage is a home loan that features relatively low payments during the initial term—often interest-only or calculated on a long amortization—followed by one large lump-sum payoff (the “balloon”) due at the end of the term. This structure can offer short‑term affordability but concentrates risk at maturity, making it suitable only for specific situations and disciplined borrowers.

How a Balloon Mortgage Works

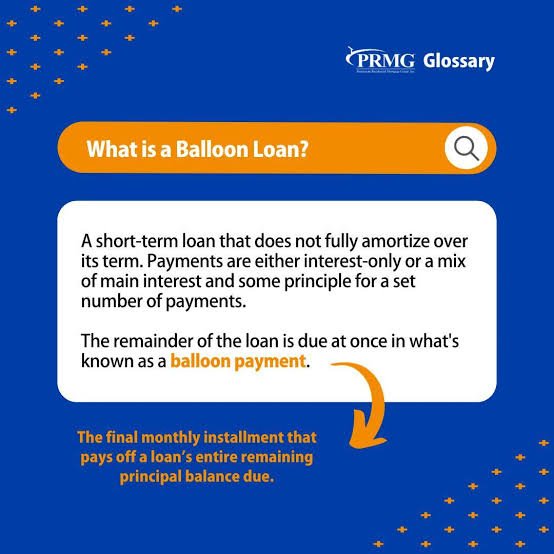

- Structure: The loan term is short (commonly 5–7 years, sometimes 10–15), while monthly payments during the term may be interest-only or based on a longer amortization (e.g., 30 years). This keeps monthly payments lower than a standard fully amortizing loan of the same size.

- The balloon payment: At maturity, any remaining principal becomes due at once. If the loan was interest‑only, nearly the entire original principal is due; if payments were partially amortizing (e.g., 30/5), the remaining balance after the scheduled payments becomes the balloon.

- Typical repayment plans: Most borrowers plan to satisfy the balloon by either refinancing into a new mortgage before maturity or selling the property. A smaller group intends to pay the lump sum from expected liquidity events (e.g., a business sale, inheritance, vesting bonuses).

- Not a negative amortization loan: Balloon loans don’t inherently increase the principal balance (that would be negative amortization). Instead, they delay paying down principal, leaving a sizable amount due later.

Key Features vs. Conventional Mortgages

- Term length: Balloon mortgages often run 5–7 years; conventional fixed-rate mortgages are commonly 15 or 30 years.

- Payment profile: Balloon loans start with lower monthly payments; conventional loans amortize, gradually shifting more of each payment to principal over time.

- Interest rates: Balloons can carry lower initial rates than comparable fixed-rate loans, contributing to lower early payments.

- End-of-term risk: Conventional mortgages fully amortize—no lump sum at the end—while balloons concentrate risk at maturity.

Pros

- Lower initial payments: Helpful for cash‑flow management, especially if income is temporarily lower or funds need to be allocated to other priorities in the short run.

- Potentially lower initial rate: Can reduce carrying costs during the early years compared with some fixed-rate alternatives.

- Flexibility for short holding periods: For buyers who expect to sell within a few years, paying less up front may be rational if the property will be disposed of before the balloon comes due.

- Often no prepayment penalties: Many balloon structures let borrowers pay extra principal to shrink the final lump sum, though this depends on the lender and jurisdiction.

Cons

- Concentrated maturity risk: A large lump sum comes due regardless of market conditions, interest rates, or personal finance shocks. If refinancing or selling isn’t feasible, default risk rises.

- Refinancing uncertainty: If credit standards tighten, property values fall, or rates rise, refinancing may be difficult or expensive when the balloon is due.

- Equity buildup is slow: With interest‑only or lightly amortizing payments, principal doesn’t fall much, leaving limited equity cushioning against price declines.

- Foreclosure risk: Inability to meet the balloon can quickly trigger serious delinquency and potential loss of the home.

Who Might Consider It

- Short-term owners: Buyers planning to sell or move within 3–7 years, who value lower payments during that window.

- Expectation of higher income: Professionals with strong, credible income growth trajectories—e.g., medical residents, associates on partnership tracks, start‑up founders with near‑term liquidity.

- Known liquidity events: Borrowers expecting a reliable lump sum—property sale proceeds, vested bonus, inheritance—timed before or at loan maturity.

- Investors and bridge scenarios: Situations where a property will be refinanced or sold after a renovation, lease‑up, or other value‑add milestone.

Who Should Likely Avoid It

- Borrowers needing long-term stability: Households seeking predictable payments and no maturity event.

- Those with thin savings or volatile income: A balloon magnifies late‑term risk; inadequate reserves heighten the danger.

- Buyers in uncertain markets: If property values might stall or fall, refinancing could become difficult when the balloon hits.

Common Structures and Terminology

- Interest‑only balloon: Pay interest monthly; full principal due at maturity.

- 30/5 or 30/7 balloon: Payments are calculated as if on a 30‑year schedule, but the loan matures in 5 or 7 years, leaving the remaining balance due then.

- Reset/conditional extension clauses: Some balloon notes include a right (subject to conditions) to reset the rate and extend the loan if the borrower meets performance and loan‑to‑value criteria; this is lender‑ and contract‑specific and not guaranteed.

Practical Risk Management

- Plan A and Plan B: Before closing, define both a primary exit (e.g., planned sale in 4–5 years) and a contingency (e.g., refinancing pathways with target credit score, DTI, and LTV).

- Prepay prudently: If allowed, channel surplus cash to principal during the term to shrink the future balloon; even modest extra payments can materially reduce the lump sum.

- Track timelines: Calendar critical dates—rate adjustments, maturity, any reset windows—at closing; set reminders 12, 9, 6, and 3 months ahead of maturity to initiate refinance or sale prep.

- Maintain strong credit: Keep utilization low, pay on time, avoid taking on new debt prior to refinance; this preserves the best rates and options.

- Watch LTV and market value: Keep tabs on local prices and property condition; consider targeted improvements that enhance appraised value before refinance.

- Build reserves: Maintain a healthy emergency fund beyond closing to cover shocks and provide flexibility near maturity.

Alternatives to Consider

- Adjustable-rate mortgage (ARM): Typically offers lower initial rates than a 30‑year fixed without a hard balloon; payments continue after the fixed period, but the rate can adjust up or down.

- Shorter fixed-term loans (e.g., 15-year): Higher monthly payments but faster amortization and no balloon risk.

- Hybrid interest‑only ARMs: Interest‑only period (e.g., 10 years) followed by amortization; payment shock risk remains, but there’s no single balloon date.

- Bridge loan with defined exit: For temporary financing tied to a known sale or liquidity event, a bridge may be more appropriate and explicit about timing.

Regulatory and Market Considerations

- Availability and terms vary: Post‑crisis underwriting tightened in many markets; not all lenders offer balloon mortgages, and those that do may require stronger credentials.

- Contract specifics matter: Balloon clauses, prepayment terms, potential resets, and any extension conditions are all determined by the note and local law—read documents carefully and seek independent advice.

- Appraisal and rate environment: Rising rates and softening values can complicate refinancing; build conservative assumptions into planning.

Example Scenario (Conceptual)

- Loan: $300,000, 30/5 balloon at a low fixed rate during the term.

- Payments: Monthly payments are calculated on a 30‑year schedule for 60 months, keeping costs modest.

- Balloon: After 60 months, the remaining principal—still the bulk of the original amount—is due at once.

- Exit: Borrower refinances into a standard mortgage at month 54–57 or lists the home for sale to close before maturity.

Due Diligence Checklist

- Confirm: Interest‑only vs. partial amortization; exact maturity date; balloon amount estimate based on the payment schedule.

- Verify: Prepayment policy; presence/terms of any reset or extension right; escrow requirements; late‑fee triggers.

- Model: Multiple refinance scenarios with higher rates and different appraisals; ensure debt‑to‑income remains within lender guidelines.

- Consult: A qualified mortgage advisor or housing counselor to evaluate suitability in light of income stability, savings, and local market conditions.

Bottom Line

A balloon mortgage can make sense for disciplined borrowers with short holding periods or reliable future liquidity, offering lower initial payments and potentially lower initial rates. The trade‑off is concentrated end‑of‑term risk: the entire remaining principal comes due regardless of market or personal circumstances. Success with a balloon mortgage hinges on credible exit planning, rigorous cash management, and conservative assumptions about refinancing and resale conditions.