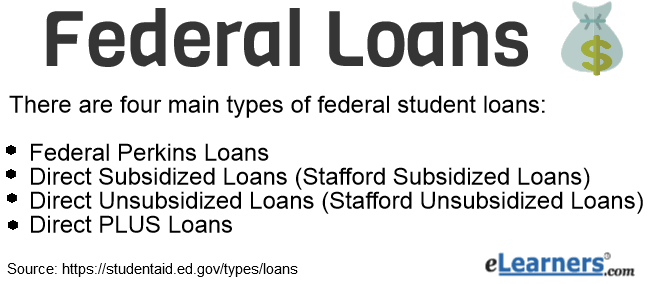

The Federal Perkins Loan was a legacy, campus-based, need-focused student loan program that offered a fixed 5% interest rate, generous deferment and cancellation benefits, and school-level servicing; authority to make new loans ended on Sept. 30, 2017, with final disbursements through June 30, 2018, though existing borrowers continue under original terms and servicing arrangements today .

What it was

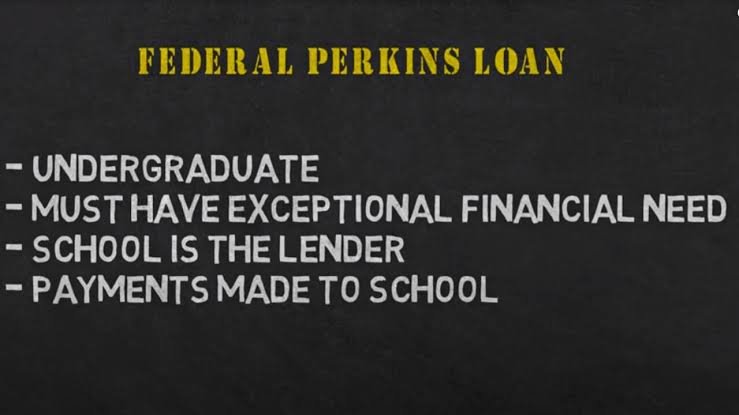

The Perkins Loan (initially the National Defense Student Loan in 1958, later National Direct Student Loan) was a federal program run in partnership with participating colleges, targeting students with exceptional financial need and supplying low-interest, subsidized loans from revolving campus funds matched by institutions and federal capital contributions . Loans were subsidized while in school and during a nine‑month grace period, meaning no interest accrued until repayment began, and then carried a fixed 5% rate with standard 10‑year amortization and minimum payments often set at $40 per month in school policies . Financial aid administrators had flexibility to package Perkins alongside grants and other loans to fill gaps for low‑ and middle‑income students when federal grant aid and other loans were insufficient .

Eligibility and limits

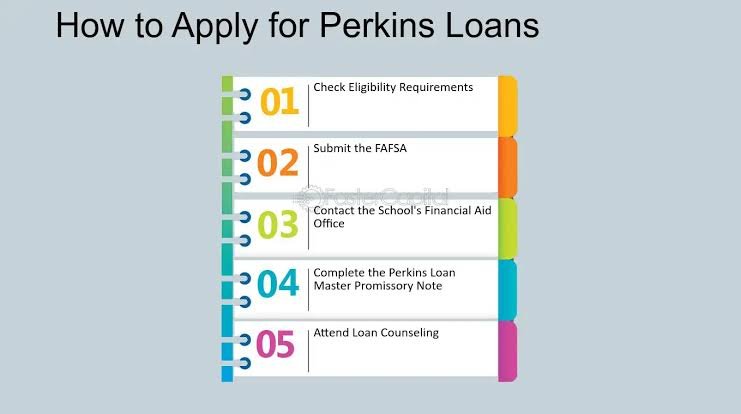

Perkins aid was awarded to at least half‑time students with exceptional financial need as determined by institutional packaging rules and federal guidance, making it distinct from entitlement-style Direct Loans; institutional discretion and limited campus fund availability meant not all eligible students received awards . Historical annual limits were typically up to $5,500$5,500 per year for undergraduates with a cumulative cap of $27,500$27,500, and up to $8,000$8,000 per year for graduate students with a lifetime cap of $60,000$60,000 including undergraduate amounts, subject to campus fund availability . Because funds were recycled through repayments, availability varied by institution and year, reinforcing the program’s campus-based, revolving-fund nature .

Interest, grace, and repayment

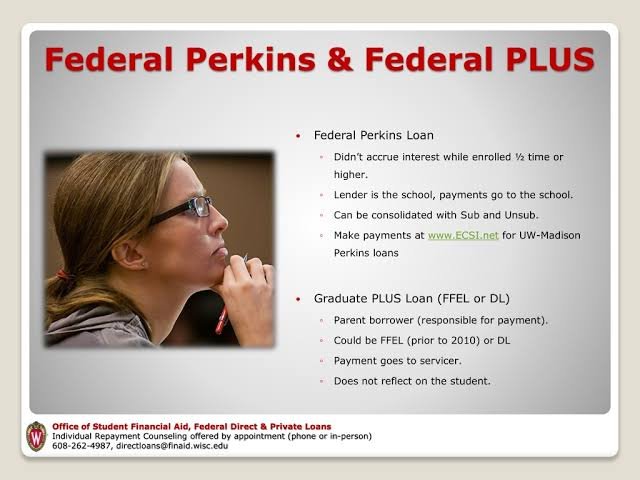

Key borrower-friendly features included a fixed 5% interest rate and a nine‑month grace period after leaving at least half‑time enrollment, after which repayment began in the tenth month, with no interest accruing during school, grace, or eligible deferment periods because the loan was subsidized . Standard repayment terms targeted a 10‑year payoff horizon with institutional servicing (often via third‑party servicers like Heartland ECSI), and minimum monthly payments set by promissory note and policy, frequently ≥$40≥$40 per month, with no prepayment penalty . Borrowers who returned to at least half‑time status after entering repayment could receive in‑school deferment on existing Perkins, though the used grace period would not reset for those same loans; new Perkins disbursed later would have their own grace .

Deferment, forbearance, and protections

Perkins offered an array of deferment categories familiar to federal borrowers (in‑school, unemployment, economic hardship, military service) during which interest did not accrue due to the subsidy, alongside administrative forbearance options when deferment criteria were not met but temporary payment relief was necessary . Schools were required to afford borrowers maximum opportunity to repay, following procedural steps for billing, outreach, and cure of delinquency before escalation, reflecting the program’s borrower-protective compliance framework . Even after the program’s sunset for new lending, these protections continue to govern outstanding Perkins portfolios under existing promissory notes and regulations .

Cancellation and discharge

A hallmark of Perkins was robust cancellation eligibility for public service and certain professions, with percentage-based cancellation accruing annually over up to five years, often 15% for years 1–2, 20% for years 3–4, and 30% for year 5, effectively eliminating the balance for sustained qualifying service . Eligible roles included teaching in low‑income schools or shortage areas, nursing, law enforcement, firefighting, early childhood education, librarians, public defenders, certain military service, and Peace Corps service, among others, with detailed criteria and documentation managed through campus servicers . Perkins also provided discharge avenues under standard federal criteria such as total and permanent disability, death, and certain school-related closures or borrower defenses as applicable under program rules .

Program sunset and current status

Congress allowed the authority for new Perkins originations to lapse on Sept. 30, 2017; schools could make final disbursements through June 30, 2018, after which no new Perkins could be awarded, though existing loans remain enforceable under original terms . Following the sunset, the Department of Education established a structured assignment and liquidation process requiring schools to assign remaining Perkins, NDSL, and Defense Loans to the Department and to liquidate revolving funds, ensuring accurate National Student Loan Data System (NSLDS) status updates and proper transfer or closure of accounts . Historically, the federal government reimbursed institutions for certain cancellation costs through appropriations, a practice that ceased after FY 2010, leaving colleges with unreimbursed cancellation exposure that became a policy issue during wind‑down .

Servicing and borrower actions today

Borrowers with outstanding Perkins typically repay the school or its contracted servicer; campus bursar or loan offices remain the first point of contact for exit counseling, billing, deferment, cancellation requests, and rehabilitation of defaults where possible . For borrowers whose loans are assigned to the Department during liquidation, servicing transitions to federal management, and borrowers should monitor communications and NSLDS records to track status, especially during cancellation or deferment processing . Federal Student Aid maintains current guidance on Perkins cancellation, discharge, deferment, and repayment options, and borrowers should use these resources alongside campus instructions to preserve eligibility and avoid delinquency .

Historical context and impact

Originating in the National Defense Education Act of 1958 amid Cold War-era education priorities, the program embodied a revolving-fund model that multiplied initial federal capital through decades of lending and repayment, with institutions matching funds and administering aid close to students . In FY 2009 alone, roughly 1,700 campuses made over $1.1$1.1 billion in Perkins loans to about 521,000 students, underscoring its scale as a gap‑filling, low‑cost borrowing option for needy populations prior to its discontinuation for new borrowers . The end of new lending shifted reliance to Direct Loans and institutional aid, while legacy borrowers retained the Perkins program’s distinctive benefits, particularly cancellation for public service and the subsidized 5% rate .