Mortgages are one of the most significant financial commitments individuals make in their lifetime. They serve as the bridge between homeownership dreams and financial reality, enabling people to purchase property without paying the full amount upfront. Understanding mortgages is essential for anyone planning to buy a home, refinance, or invest in real estate.

What is a Mortgage?

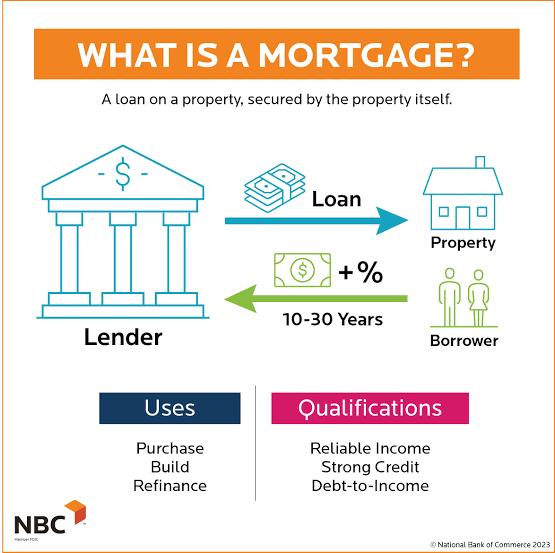

A mortgage is essentially a loan provided by a bank, credit union, or financial institution to help individuals buy a home. The borrower agrees to repay the loan over a set period, typically ranging from 15 to 30 years, with interest. The property itself acts as collateral, meaning the lender can repossess it if the borrower fails to meet repayment obligations.

Types of Mortgages

- Fixed-rate mortgage: The interest rate remains constant throughout the loan term, offering stability and predictability.

- Adjustable-rate mortgage: The interest rate fluctuates based on market conditions, often starting lower but carrying future risk.

- Government-backed loans: Programs like FHA, VA, or USDA loans provide support to first-time buyers, veterans, or rural residents.

- Interest-only mortgage: Borrowers pay only interest for a set period before principal payments begin.

Key Components of Mortgages

- Principal: The original loan amount borrowed.

- Interest: The cost of borrowing money, determined by the interest rate.

- Taxes: Local property taxes often included in monthly payments.

- Insurance: Homeowners insurance and sometimes mortgage insurance to protect lenders.

Factors Influencing Mortgage Approval

- Credit score: Higher scores lead to better interest rates.

- Income stability: Lenders assess job history and income consistency.

- Debt-to-income ratio: Determines how much of your income goes toward debt.

- Down payment: Larger down payments reduce loan size and risk.

Mortgages in the Global Context

Mortgages vary worldwide depending on financial systems and housing markets. For example:

- In the U.S., 30-year fixed-rate mortgages are common.

- In the U.K., shorter terms and variable rates dominate.

- In countries like Germany, long-term fixed mortgages are rare, with shorter repayment cycles preferred.

Benefits and Risks of Mortgages

- Benefits:

- Enables homeownership without full upfront payment.

- Builds equity over time.

- Potential tax deductions on interest payments.

- Risks:

- Long-term financial commitment.

- Risk of foreclosure if payments are missed.

- Interest rate fluctuations for adjustable loans.

Conclusion: Summary

Mortgages are powerful financial tools that make homeownership accessible to millions. They combine principal, interest, taxes, and insurance into manageable monthly payments, tailored to individual financial situations. Choosing the right mortgage requires careful consideration of loan type, interest rates, and personal financial health. While mortgages open the door to stability and investment, they also demand responsibility and foresight. In essence, understanding mortgages is the first step toward building a secure and prosperous future.