Auto loans are one of the most common financial products used by individuals to purchase vehicles without paying the full amount upfront. They provide access to funds that cover the cost of a car, allowing borrowers to repay the loan over time with interest. Understanding auto loans, their types, repayment options, and long-term impact is essential for making smart financial decisions.

What Are Auto Loans?

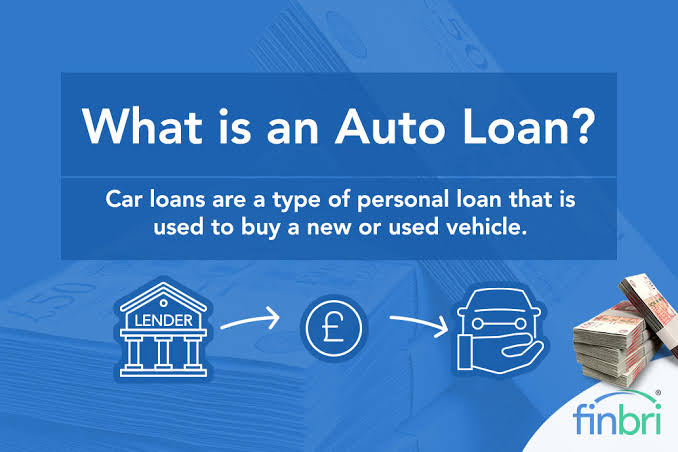

An auto loan is a type of installment loan where a lender provides money to purchase a vehicle, and the borrower agrees to repay it in fixed monthly payments over a set period. Unlike personal loans, auto loans are usually secured by the vehicle itself, meaning the lender can repossess the car if payments are not made.

Types of Auto Loans

- Bank Auto Loans: Offered by traditional banks with competitive interest rates, often requiring strong credit.

- Credit Union Loans: Known for lower rates and flexible terms, especially for members.

- Dealer Financing: Convenient but sometimes comes with higher interest rates.

- Online Lenders: Provide quick approvals and competitive offers, often appealing to tech-savvy borrowers.

Key Factors to Consider

- Interest Rates: Rates vary depending on credit score, loan term, and lender.

- Loan Term: Shorter terms mean higher monthly payments but less interest overall.

- Down Payment: A larger down payment reduces the loan amount and interest burden.

- Credit Score: Higher scores unlock better rates and terms.

Pros and Cons of Auto Loans

Advantages:

- Immediate access to a vehicle.

- Flexible repayment options.

- Builds credit history with timely payments.

Disadvantages:

- Interest costs increase the total price of the car.

- Risk of repossession if payments are missed.

- Long-term debt commitment.

Repayment Strategies

- Biweekly Payments: Helps reduce interest and pay off faster.

- Refinancing: Can lower monthly payments if interest rates drop.

- Extra Payments: Paying more than the minimum reduces principal faster.

Impact on Financial Health

Auto loans can strengthen financial standing if managed responsibly. Timely payments improve credit scores, while missed payments can damage credit and lead to repossession. Borrowers should balance affordability with necessity, ensuring the loan does not strain their budget.

Conclusion: Summary

Auto loans are a practical way to finance vehicle purchases, offering flexibility and accessibility to millions of borrowers. By understanding loan types, repayment strategies, and the impact on financial health, individuals can make informed decisions that align with their long-term goals. A well-managed auto loan not only provides mobility but also contributes positively to financial stability.